Private Equity isn't coming to save your SaaS startup. Why?

Last week, I posted about the SaaS-pocalypse and the impact of the collapsing seat economy on venture investment in many SaaS startups.

Perhaps instead of raising another round, the best path is the sale to Private Equity?

Not so fast.

📉 The Over-Exposure Problem

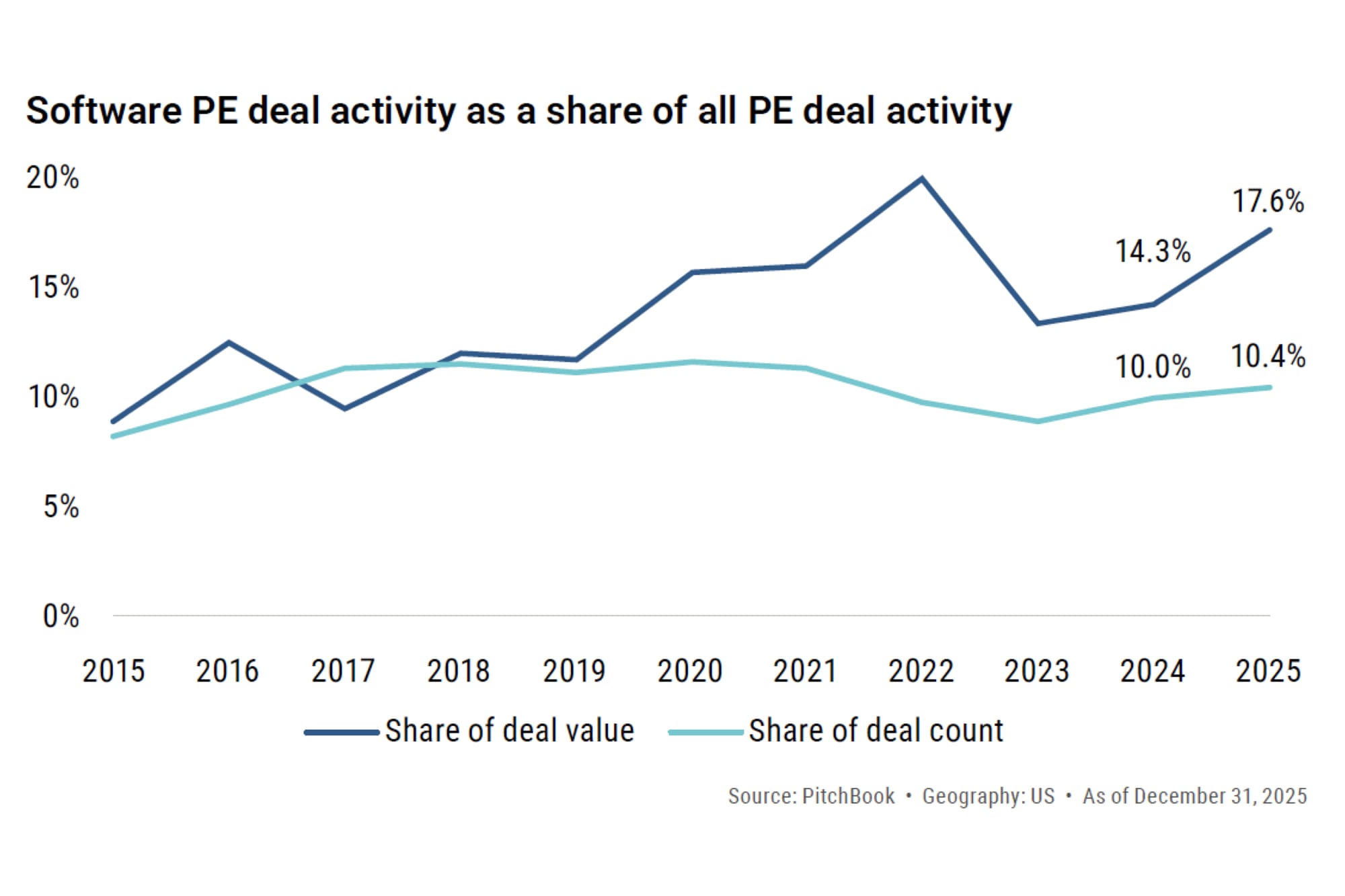

In 2025, Private Equity firms didn't pull back from software. They doubled down.

According to the data, software deal value jumped to 17.6% of all US PE deal activity last year. That is up from 14.3% the year prior.

In total, PE firms loaded their portfolios with $203.3 billion in software assets in a single year. They concentrated their bets. They filled their bags.

📉 The Valuation Rug Pull

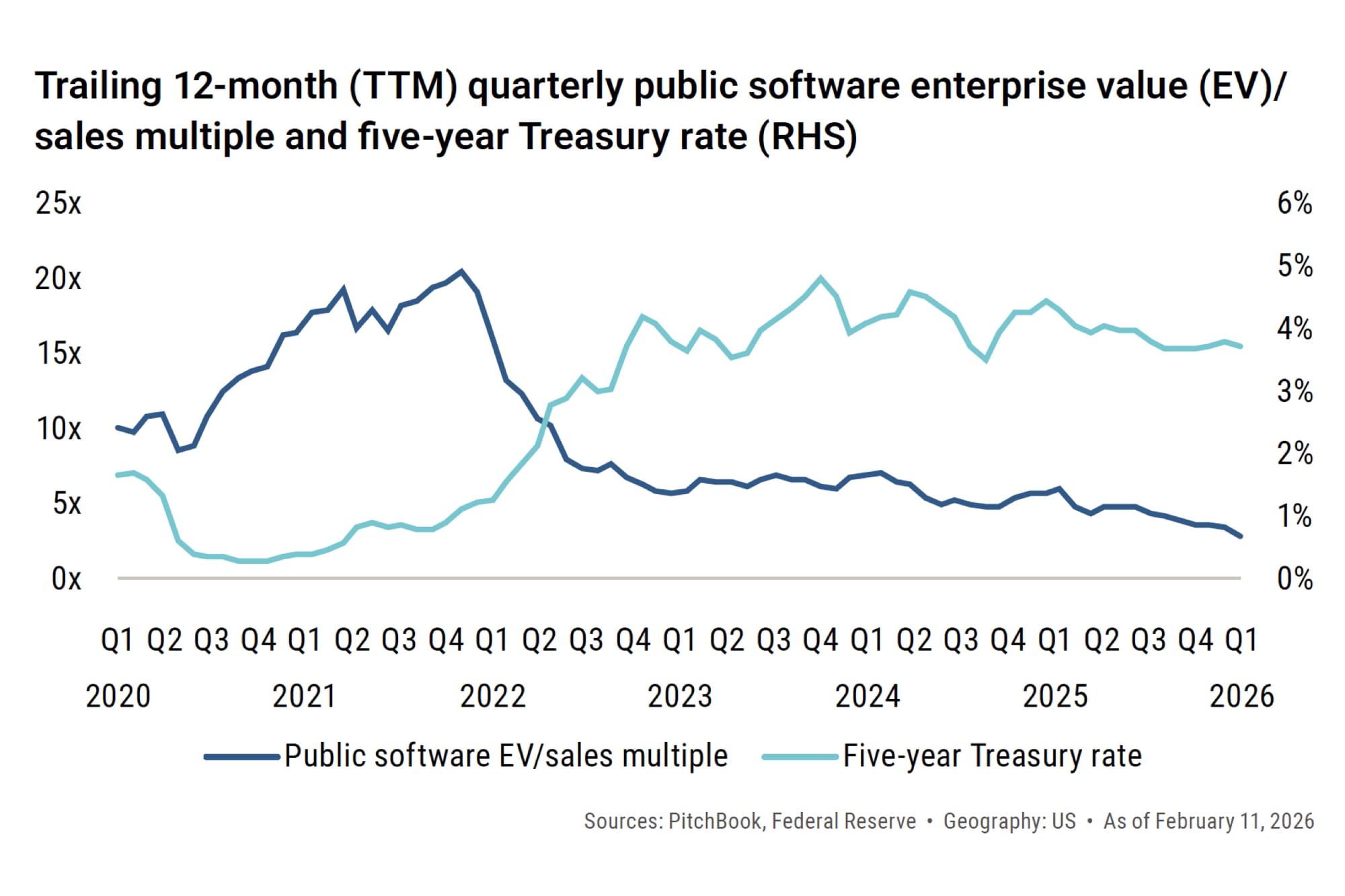

Right as PE firms concentrated their exposure, the public market—which determines the exit price for these assets—decided software was toxic.

Look at the public software valuations. They didn't just dip. They crashed through the floor.

Public multiples have dropped below the "-1 Standard Deviation" line relative to their eight-year average.

The market is no longer pricing software for "growth." It is pricing it for "disruption risk."

👉 This creates a liquidity trap.

PE firms are holding a massive portfolio of software assets that are currently underwater relative to historical exit multiples. They bought a record amount of inventory right before the market decided that this inventory was distressed.

They aren't looking to add more "risk" to a portfolio that is already flashing red.

If you are a founder waiting for a PE buyout, you need to change your pitch immediately.

1️⃣ Stop pitching "High Burn - High Growth".

PE firms are currently allergic to high-burn growth stories. They have enough of that risk on their books. The winners will show strong unit economics, low churn, and a cash-efficient growth flywheel.

2️⃣ Pitch "Indispensability".

You must prove you are a System of Record, not just a workflow tool. If your software can be replaced by a generic AI agent in 6 months, you are "thin-moat" and uninvestable.

You must own the proprietary data (the history, the compliance logs, the customer records). Show Switching Costs. Show that ripping you out would require retraining the entire workforce or risking a compliance audit.

3️⃣ Kill your 2021 benchmarks.

If you are anchoring your valuation expectations to the last cycle, you are hallucinating. The public market is trading at a standard deviation below the average. That is your new reality.

Private Equity isn't a savior. It's a stressed-out asset manager trying to fix a lopsided portfolio.

Startups that adjust accordingly will be attractive acquisition targets that help PE dig out of this hole.

Sources and Further Reading

Whenever you are ready, here is how I can help:

🖥️ Work with me: I help founders take charge of their startup's destiny. See my services here.

📫 Have a specific question about this post? Just hit reply.

You can follow me on LinkedIn or RSS.